Financial Accounts first quarter 2023

Households withdraw money from bank accounts and borrow less and less (corrected 2023-06-16)

Statistical news from Statistics Sweden 2023-06-15 8.00

Households’ margins are being squeezed by higher costs and lower real wages. The growth rates of assets in bank accounts and loans were low. Deposits in bank accounts were negative for the second consecutive quarter, something not previously noted in Financial Accounts.

Correction: The balance and transaction for pension rights, traditional, have been revised for 2021kv1-2022kv4 after an incorrect publication in SSD on 15/06. This affects sector S129, counter-sector S14 and account item FL6301, which means that household savings has been affected. The cause was a system malfunction.

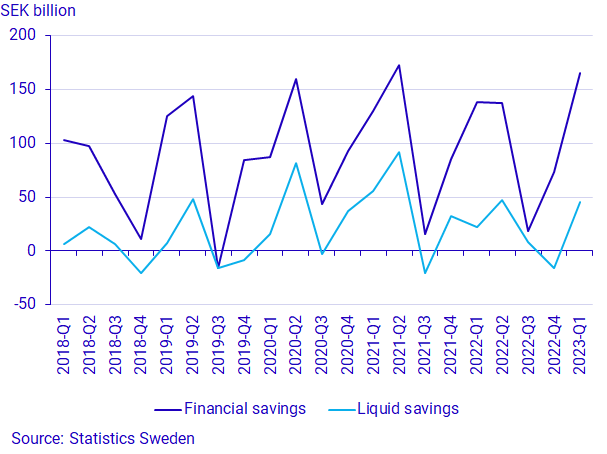

Household liquid savings amounted to SEK 45 billion for the first quarter of 2023. This is SEK 23 billion higher than the corresponding quarter last year. This was raised by the fact that the first electricity subsidy of SEK 17 billion came into household bank accounts. High inflation, which has created low real wages and high interest rates, has put downward pressure both on households' willingness to borrow and their assets in bank accounts.

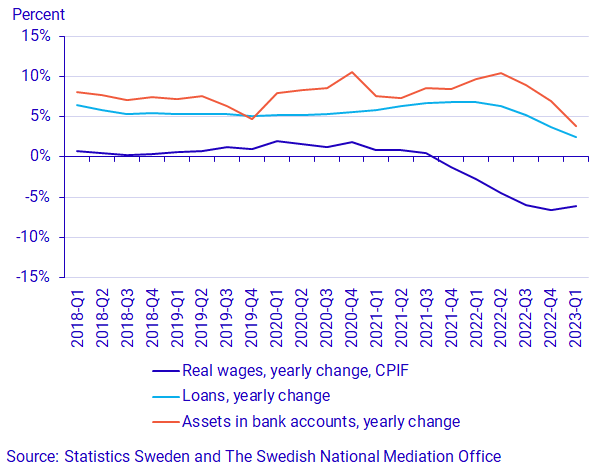

The graph below shows real wage developments as well as the annual growth rates of loans and assets in bank accounts. Annual growth rates for loans and bank account assets for the first quarter of 2023 were remarkably low at 2.5 and 3.9 percent respectively. The growth rate in loans was the lowest in the time series and to find a lower growth rate for assets in bank accounts, we must go back to the beginning of 2010.

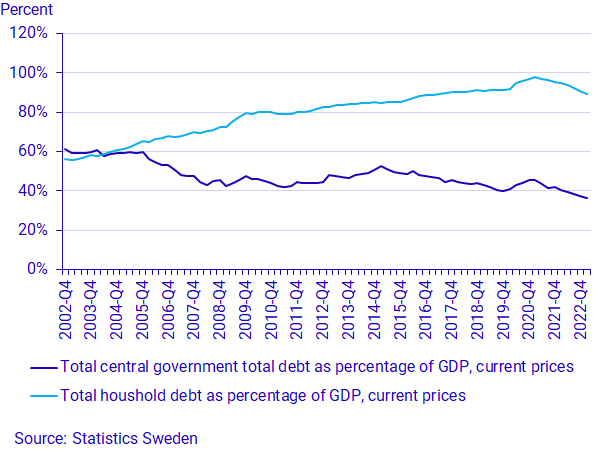

Declining household borrowing is also visible in household debt-to-GDP ratio. The development of nominal GDP has been relatively strong since the start of the period of high inflation, which has pushed down household debt-to-GDP ratio.

The central government debt ratio has also fallen after the phasing out of financial corona support measures and a relatively restrictive fiscal policy, also linked to the level of inflation.

Net withdrawals from household bank accounts for the second consecutive quarter

During the quarter, households net purchased listed shares for SEK 7 billion and fund shares to a value of SEK 16 billion.

Bank deposits were negative for the second consecutive quarter and amounted to SEK -11 billion, which is SEK 67 billion less than during the same period last year.

At the end of the quarter, household total loans amounted to SEK 5,214 billion, corresponding to an annual growth rate of 2.5 percent.

Household net borrowing during the quarter amounted to SEK 7 billion. This is SEK 62 billion less than during the same period last year.

Household financial savings, which in contrast to liquid savings include pensions and tax accruals, amounted to SEK 167 billion.

Turbulence in the banking sector

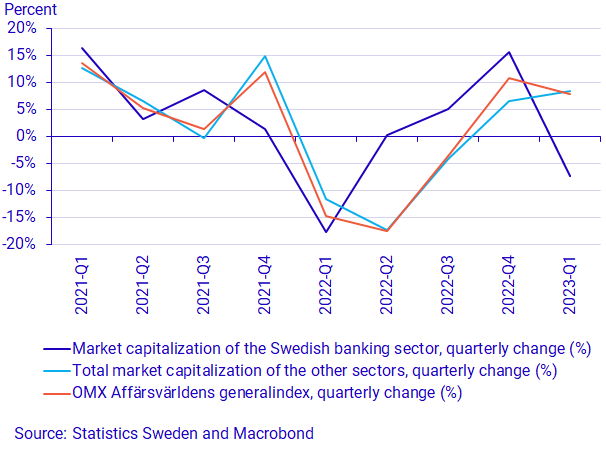

The major Swedish banks had a tough quarter on the stock exchange. While the Stockholm stock exchange rose 7.9 percent in the first quarter of 2023, the shares of the big Swedish banks fell by 5.1 percent on average. The Swedish banking sector, of which the big banks make up the largest part, saw its market capitalization decline during the quarter, from SEK 683 billion to SEK 633 billion. Other sectors, i.e., excluding the banking sector, increased by 8.3 per cent to a total capitalization of SEK 13,982 billion at the end of the quarter.

At the end of the first quarter of 2023, the stock market was characterized by a great deal of concern linked to the financial sector, which was triggered by the collapse of Silicon Valley Bank in the United States in March. This also spread to other US banks after it was discovered that more of them had liquidity problems. Europe was also affected, with the takeover of a distressed European bank putting the stability of the banking system in question. The share prices of the major Swedish banks fell at the end of the quarter because of broad uncertainty in the sector.

Non-financial corporations financed themselves through loans

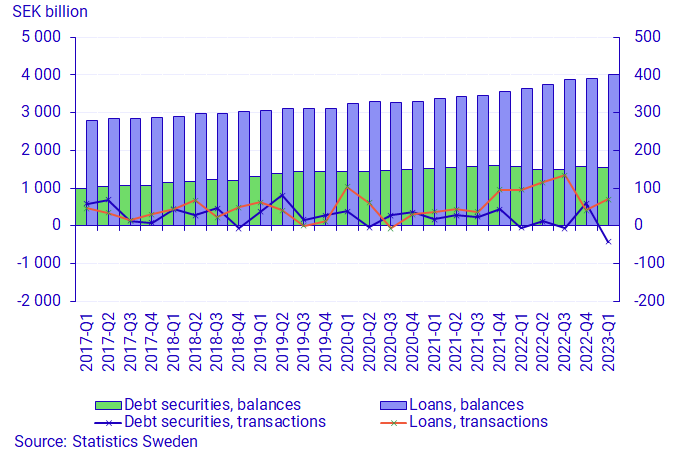

During the first quarter of 2023, non-financial companies financed themselves through loans, newly taken minus amortized, to a value of SEK 70 billion. This is more than in the previous quarter but less than in the corresponding quarter of the year before. Financing through debt securities decreased and net issues, new issues minus maturities and repurchases, amounted to SEK -43 billion. This is the lowest financing via debt securities since the start of the time series. Debt financing remained the largest form of financing and total loans amounted to SEK 4,002 billion, compared with SEK 1,541 billion for debt securities.

Revisions

In connection with the calculation of the first quarter of 2023, annual and quarterly statistics have been revised for the period 2021Q1-2022Q4. The rest of the world sector has been revised as of the first quarter of 2021 with new information from the Balance of Payments.

Definitions and explanations

The purpose of financial accounts is to provide information on financial assets and liabilities as well as changes in net lending and financial assets for different sectors of society.

The net lending of financial accounts is calculated as the difference between transactions in financial assets and transactions in liabilities. In real Sector Accounts, which, like Financial Accounts, is part of National Accounts, net lending is calculated as the difference between income and expenses. However, financial accounts and real sector accounts are based on different sources, which gives rise to differences between products.

In Financial Accounts, public debt is calculated differently from the most commonly reported measure of government debt, which is calculated according to the convergence criteria, the so-called Maastricht debt. The definition of the Maastricht debt does not include all financial instruments, the instruments are presented at nominal value and the liabilities for government administration are consolidated. Central government debt in Financial Accounts is not consolidated and includes all financial instruments at market value.

In addition to central government, the state administration sector also includes certain state foundations and certain state-owned companies. State administration does not include units of the old-age pension system. Instead, they constitute the social security funds sector. Municipal administration includes primary municipal authorities, regional authorities (formerly county councils), municipal associations, as well as some municipal foundations and certain municipally or regionally owned companies.

Real wage development is taken from the Mediation Institute's Economic Wage Statistics, which uses data from Statistics Sweden. Real wages are derived from nominal wages deflated with CPIF. The figures in this statistical news are the average of the monthly figures that make up each quarter.

Sea information: Nationalförmögenheten

In connection with the publication of Financial Accounts, the National Wealth Report is also published, which contains annual data on both real and financial assets. The financial assets and liabilities are derived from the Financial Accounts and are thus consistent with the values published in the Financial Accounts.

For further information, see:

Nationalförmögenheten och nationella balansräkningar (in Swedish) (pdf)

Next publishing will be

The next statistical news in this series is scheduled for publishing on 2023-09-21 at 08.00

Feel free to use the facts from this statistical news but remember to state Source: Statistics Sweden.